Key Takeaways

- e-Invoice is mandatory for businesses with turnover above Rs 5 crore in any financial year since 2017-18.

- Businesses with turnover above Rs 10 crore must report invoices to the IRP within 30 days of the invoice date.

- e-Way Bill is required for consignments above Rs 50,000 moving interstate, with validity calculated at 1 day per 200 km.

- An invoice without a valid IRN and QR code is legally invalid and can block the buyer from claiming ITC.

- When turnover crosses Rs 5 crore, the IRP auto-populates Part A of the e-Way Bill from e-invoice data.

- Non-compliance with e-Way Bill rules carries a minimum penalty of Rs 10,000 or the tax evaded, whichever is higher.

Rs 5 Cr

turnover threshold that triggers mandatory e-invoicing in 2026

30 days

window for Rs 10 crore+ businesses to report invoices to the IRP

200%

of tax payable as maximum penalty under Section 129 for e-Way Bill violations

Most business owners hear e-Invoice and e-Way Bill in the same sentence and assume they are two names for the same thing. They are not. Both are mandatory under GST, both use invoice data, but they serve different legal purposes, apply to different thresholds, and carry different penalties.

This guide separates the two clearly, explains each from scratch, covers 2026 rule updates, and shows how the systems connect when your turnover crosses the applicable threshold.

01What is e-Invoice under GST?

An e-Invoice is not a PDF emailed to a customer. It is an invoice registered on a Government-notified Invoice Registration Portal and returned with a unique Invoice Reference Number and digitally signed QR code.

Your software creates the invoice, sends invoice data to the IRP in JSON format, receives the 64-character IRN, and prints or shares the authenticated invoice. Without a valid IRN, an eligible B2B invoice is legally invalid under GST and the buyer cannot claim Input Tax Credit.

02What is an e-Way Bill?

An e-Way Bill is an electronic document that must accompany qualifying goods in transit. It acts like a digital transit pass and records who is sending goods, who is receiving them, what is being sent, and how it is being transported.

Form EWB-01 has two parts. Part A captures invoice and consignment details. Part B captures transport details such as vehicle number, transport mode, and distance. Validity begins only after Part B is completed.

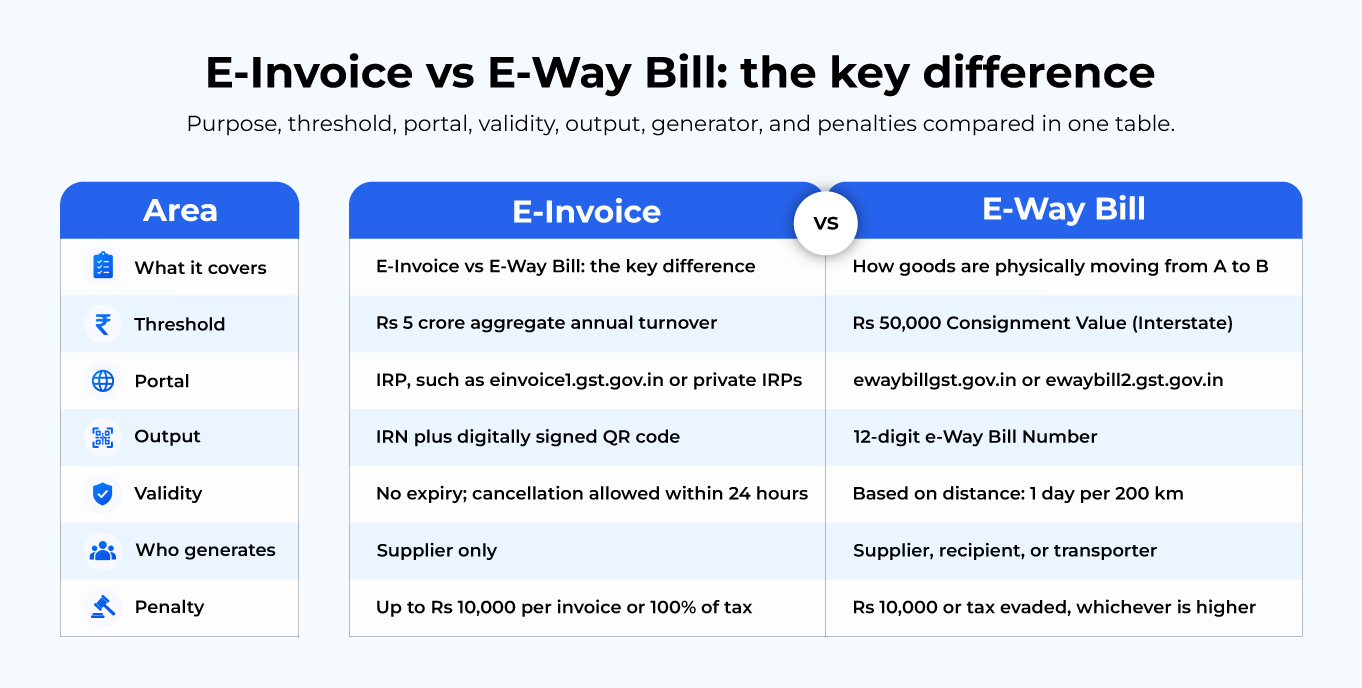

03e-Invoice vs e-Way Bill: the key difference

Infographic Zone

e-Invoice vs e-Way Bill: Side-by-Side

Purpose, threshold, portal, validity, output, generator, and penalties compared in one table.

| Area | e-Invoice | e-Way Bill |

|---|---|---|

| What it covers | Who is selling and what GST transaction is happening | How goods are physically moving from A to B |

| Threshold | Rs 5 crore aggregate annual turnover | Rs 50,000 consignment value for interstate movement |

| Portal | IRP, such as einvoice1.gst.gov.in or private IRPs | ewaybillgst.gov.in or ewaybill2.gst.gov.in |

| Output | IRN plus digitally signed QR code | 12-digit e-Way Bill Number |

| Validity | No expiry; cancellation allowed within 24 hours | Based on distance: 1 day per 200 km |

| Who generates | Supplier only | Supplier, recipient, or transporter |

| Penalty | Up to Rs 10,000 per invoice or 100% of tax | Rs 10,000 or tax evaded, whichever is higher |

A service-only business above Rs 5 crore needs e-Invoices but no e-Way Bills. A manufacturer below Rs 5 crore shipping goods above Rs 50,000 needs an e-Way Bill but not an e-Invoice. A distributor above Rs 5 crore shipping interstate goods above Rs 50,000 usually needs both.

04Who must generate e-Invoices in 2026?

In 2026, e-invoicing is mandatory for every GST-registered business whose Aggregate Annual Turnover exceeded Rs 5 crore in any financial year from 2017-18 onwards. If your business crossed Rs 5 crore even once since 2017-18, eligible transactions require IRN-authenticated invoices today.

From 1 April 2025, businesses with AATO of Rs 10 crore or more must report invoices to the IRP within 30 days of invoice date. After that window, the IRP rejects the invoice and will not generate an IRN.

Exempt categories

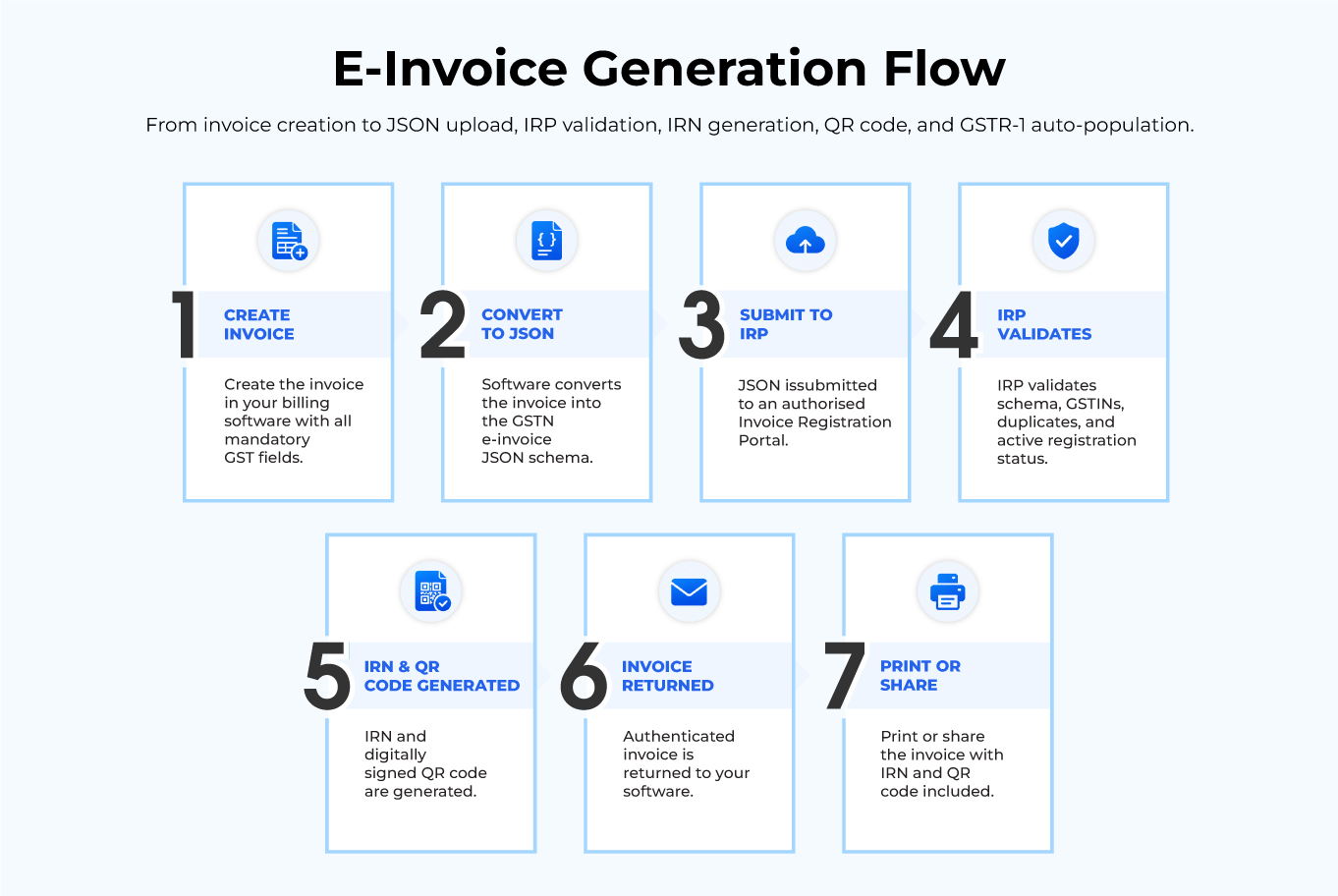

05How to generate an e-Invoice: step by step

Infographic Zone

e-Invoice Generation Flow

From invoice creation to JSON upload, IRP validation, IRN generation, QR code, and GSTR-1 auto-population.

- 1Create the invoice in your billing software with all mandatory GST fields.

- 2Software converts the invoice into the GSTN e-invoice JSON schema.

- 3JSON is submitted to an authorised Invoice Registration Portal.

- 4IRP validates schema, GSTINs, duplicates, and active registration status.

- 5IRN and digitally signed QR code are generated.

- 6Authenticated invoice is returned to your software.

- 7Print or share the invoice with IRN and QR code included.

06Who must generate e-Way Bills in 2026?

An e-Way Bill is mandatory for any consignment whose value exceeds Rs 50,000 before the goods begin moving. This applies uniformly to interstate movement across India. For intrastate movement, state thresholds may vary.

Delhi requires intrastate e-Way Bills above Rs 1,00,000. Rajasthan follows Rs 2,00,000 within city limits and Rs 1,00,000 between cities. Most other states, including Gujarat, follow the central Rs 50,000 limit.

When an e-Way Bill is not required

07e-Way Bill validity and extension rules

A 350 km consignment gets 2 days of validity. An 800 km consignment gets 4 days. If goods cannot be delivered within validity because of natural calamity, law and order issues, or transhipment delays, extensions can be requested 8 hours before or after expiry.

From January 2025, the maximum extension cap is 360 days from the original generation date. The portal also blocks e-Way Bill generation for invoices, credit notes, or delivery challans dated more than 180 days before generation.

08How e-Invoice and e-Way Bill connect

For businesses above Rs 5 crore, generating an e-Invoice sends invoice data to the e-Way Bill portal and auto-populates Part A. The dispatch team only adds Part B details such as vehicle number, transport mode, and distance before goods move.

Want T7 ERP to handle this automatically?

Auto GSTR-1, GSTR-2B reconciliation, e-Invoice, and e-Way Bill in one platform built for Indian retailers.

092026 rule updates you must know

Mandatory multi-factor authentication

From 1 April 2025, MFA is mandatory for GST portal, IRP, and e-Way Bill portal access.

e-Way Bill 2.0 portal

ewaybill2.gst.gov.in operates alongside the original portal and syncs in real time.

Automated blocking for non-filers

Businesses with inactive GSTINs or pending returns can be blocked from generating e-Way Bills.

Duplicate bill prevention

The portal blocks multiple e-Way Bills for the same invoice and date.

10Penalties for non-compliance

Missing or incorrect e-Invoices can attract a penalty of Rs 10,000 per invoice or 100% of the tax due, whichever is higher. The buyer also loses the right to claim ITC until a valid invoice is issued.

Transporting goods without a valid e-Way Bill carries a penalty of Rs 10,000 or the tax sought to be evaded, whichever is higher. In detention cases, the penalty can rise to 200% of the applicable tax payable.

e-Invoice and e-Way Bill mistakes to avoid

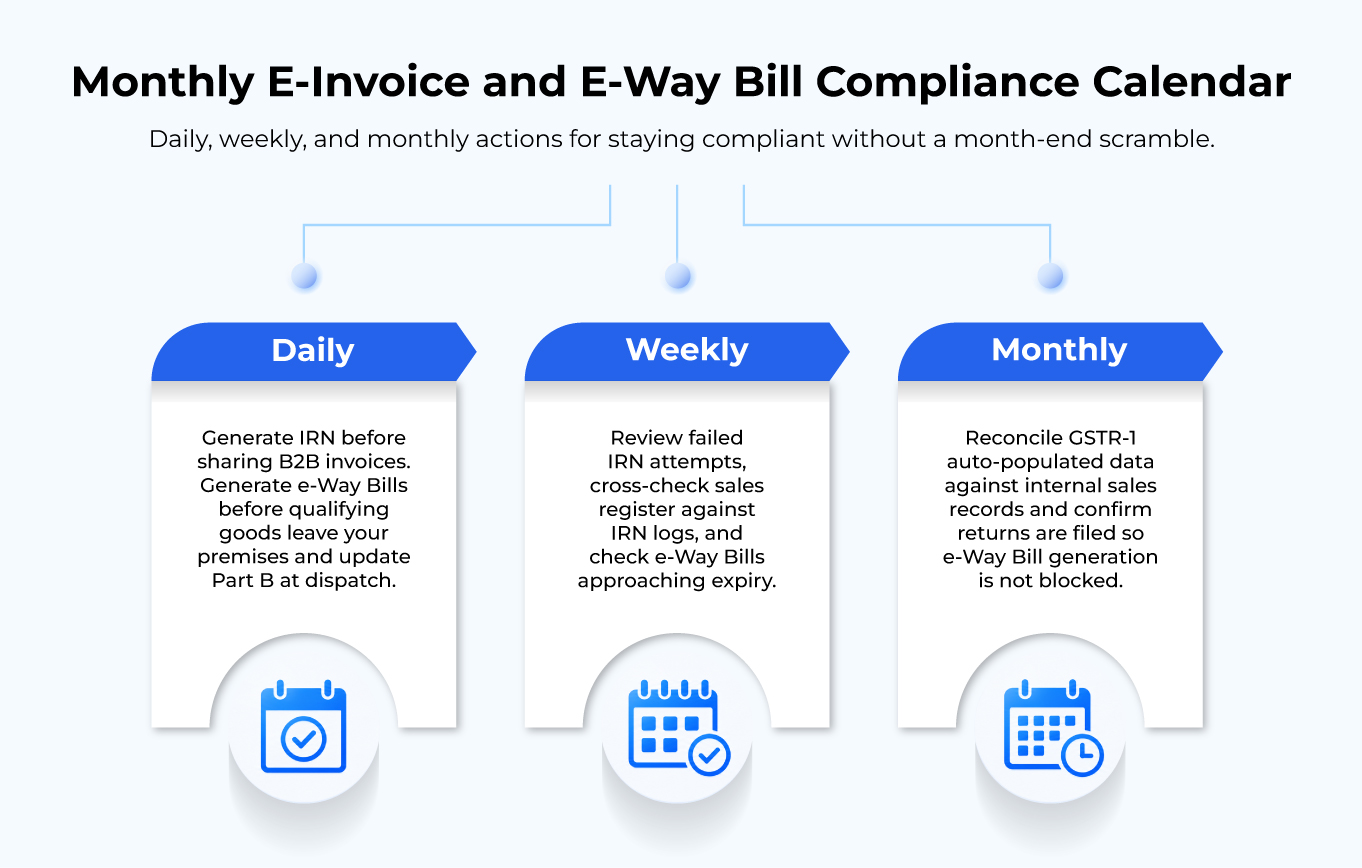

A practical monthly compliance rhythm

Infographic Zone

Monthly e-Invoice and e-Way Bill Compliance Calendar

Daily, weekly, and monthly actions for staying compliant without a month-end scramble.

Daily

Generate IRN before sharing B2B invoices. Generate e-Way Bills before qualifying goods leave your premises and update Part B at dispatch.

Weekly

Review failed IRN attempts, cross-check sales register against IRN logs, and check e-Way Bills approaching expiry.

Monthly

Reconcile GSTR-1 auto-populated data against internal sales records and confirm returns are filed so e-Way Bill generation is not blocked.

How T7 ERP handles e-Invoice and e-Way Bill

T7 ERP integrates with IRP APIs and the e-Way Bill portal. When you generate a sale invoice, the system submits it to the IRP, retrieves the IRN and QR code, and prints both on the final invoice. For qualifying consignments, Part A of the e-Way Bill is auto-populated from the same invoice data.

T7 ERP also tracks IRN status, flags invoices approaching the 30-day reporting window for businesses above Rs 10 crore, and alerts teams if e-Way Bill validity is nearing expiry for open shipments.

Want T7 ERP to handle this automatically?

Auto GSTR-1, GSTR-2B reconciliation, e-Invoice, and e-Way Bill in one platform built for Indian retailers.

Official sources and references

Conclusion

e-Invoice and e-Way Bill are two separate compliance requirements that share invoice data. One authenticates the transaction. The other authorises movement of goods. The 2026 rules make manual handling increasingly risky, so getting both documents right before goods move is now the only dependable workflow.

For current GST rates, thresholds, and regulatory updates, always verify details with CBIC, the GST Portal, or your tax advisor before filing or making compliance decisions.

Rahul Kulkarni

GST & Compliance Expert · T7 ERP

Rahul has 9 years of experience helping Indian SMBs navigate GST compliance, e-Invoice workflows, and ERP implementation. He has worked with 200+ retailers and writes practical guides for business owners who want to stay compliant without needing a CA for every question.

Related Articles

The Ultimate GST Billing Checklist for Indian Retailers in 2026

12 min read

Why Your ERP Is Making You Slower (And What to Do About It)

7 min read

Reduce Dead Stock and Overordering with AI Inventory Management

7 min read

WhatsApp for Business: How Indian Retailers Are Using It to Sell More

7 min read